In December 2023, a 33-year-old woman in the United Kingdom became the first person in the world to receive a government-approved medicine that worked by cutting her own DNA and letting it heal differently. The drug was exagamglogene autotemcel — CASGEVY — and the disease was sickle cell disease, a single-letter mutation in the beta-globin gene that has caused generations of pain crises, organ damage, and early death, disproportionately in people of African and Middle Eastern descent. CASGEVY does not correct that mutation. It does something more oblique and, in its way, more elegant: it uses CRISPR/Cas9 to disable a genetic switch called BCL11A, which normally silences fetal haemoglobin production after infancy. Switch it off, and the bone marrow reverts to making the fetal form of haemoglobin that sickled cells cannot form. The disease is not cured at the level of the mutation. It is routed around.

That approval — and the American one that followed six weeks later for both sickle cell disease and transfusion-dependent beta-thalassemia — was the moment gene editing stopped being a Nobel Prize (Jennifer Doudna and Emmanuelle Charpentier shared the 2020 Chemistry prize for CRISPR/Cas9 itself) and became a National Drug Code. Two companies own that moment jointly: Vertex Pharmaceuticals (NASDAQ: VRTX), the specialty pharma that manufactures, distributes, and books the revenue, and CRISPR Therapeutics (NASDAQ: CRSP), the platform company that discovered and designed the edit. Three and a half years later, both companies are still trading on the promise of that approval, but the market has started asking a much less romantic question than "does the science work." It is asking: does the business work? This piece is my attempt to answer that as precisely as the public data allow — for both companies individually, and for the wider genomic medicine sector they anchor.

1. What Genomic Medicine Actually Is, Mechanistically

It is worth being precise about vocabulary before going further, because "gene therapy" and "gene editing" get used interchangeably in the financial press and they are not the same thing. Gene therapy, in the older sense — the AAV-delivered replacement genes that built companies like Bluebird Bio — adds a working copy of a gene without touching the broken one. Gene editing changes the sequence that is already there. CRISPR/Cas9, the tool underlying CASGEVY, works by using a short guide RNA to direct the Cas9 enzyme to a specific DNA sequence, where it cuts both strands. The cell's own double-strand-break repair machinery then either disrupts the target gene (as in CASGEVY's BCL11A knockout) or, with a repair template supplied alongside, inserts a specific new sequence.

That double-strand break is also CRISPR/Cas9's main liability. Break repair is imprecise; it can produce unintended insertions, deletions, or — in rare but real cases — chromosomal rearrangements at or near the cut site. Two newer editing chemistries were developed explicitly to avoid this. Base editing, pioneered by David Liu's lab and commercialised by Beam Therapeutics (which Liu co-founded alongside Feng Zhang and Keith Joung), fuses a catalytically impaired Cas9 to a deaminase enzyme that chemically converts one DNA base to another — C to T, or A to G — directly, without ever cutting both strands. It is more surgical but more limited: base editors can only make transition mutations (purine-to-purine or pyrimidine-to-pyrimidine swaps), not the full range of possible single-letter changes. Prime editing, a more recent invention from the same lab, fuses a Cas9 nickase to a reverse transcriptase and uses an extended guide RNA as a template, functioning as a genomic "search and replace" that can execute all twelve possible base transitions and transversions as well as small insertions and deletions — the broadest editing vocabulary of the three, and the least clinically mature.

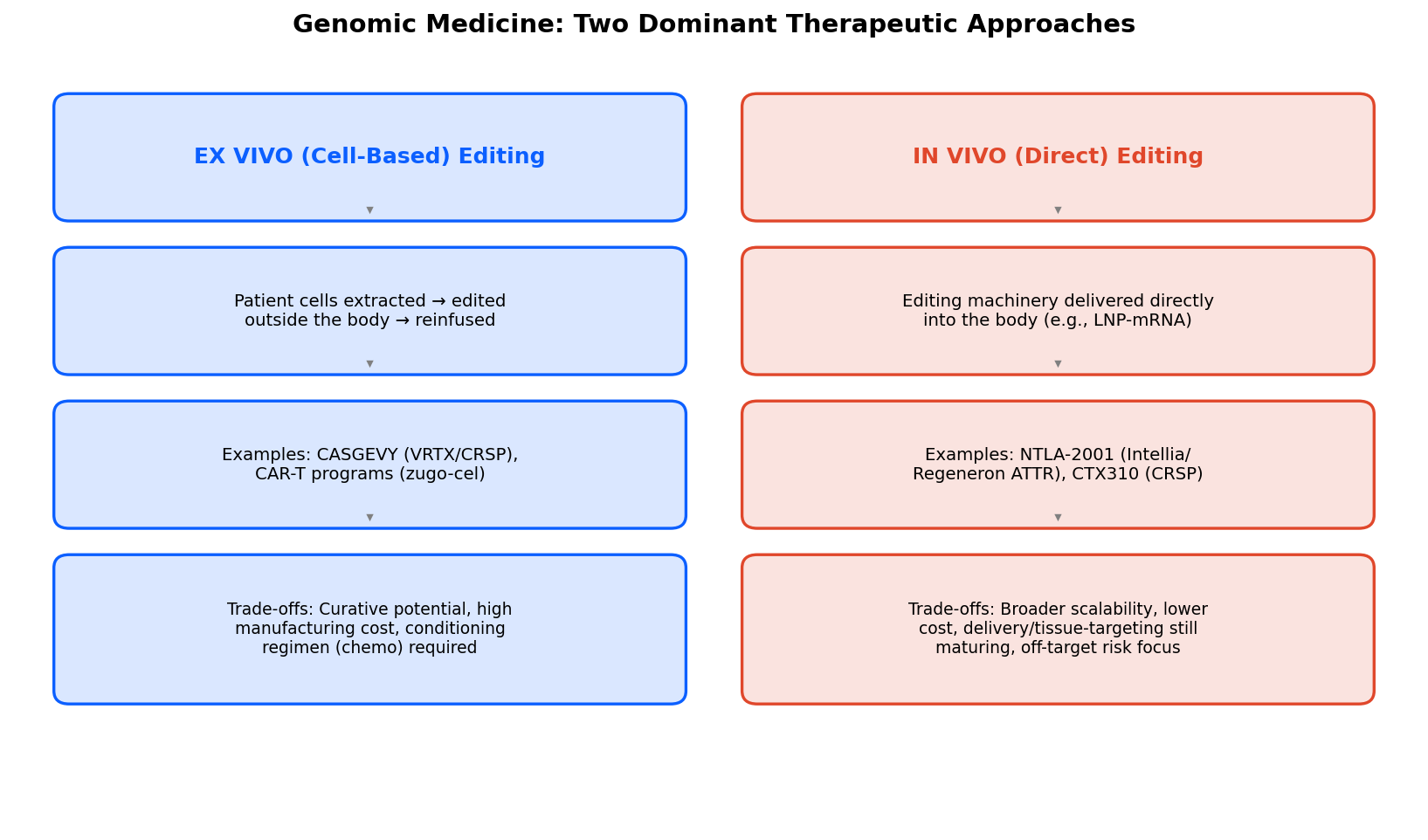

The second axis that matters as much as editing chemistry is delivery, illustrated below.

Ex vivo editing dominates approved and late-stage programs today; in vivo editing is the primary axis of competition for the next wave.

Ex vivo editing — CASGEVY's approach — extracts a patient's own haematopoietic stem cells, edits them outside the body in a manufacturing facility, and reinfuses them after the patient has undergone myeloablative conditioning (essentially, chemotherapy to clear existing bone marrow so the edited cells can engraft). This is why a CASGEVY treatment episode takes four to six months from apheresis to discharge, requires a small number of specialised Qualified Treatment Centers, and carries an all-in cost of care closer to $3 million once conditioning, hospitalisation, and monitoring are added to Vertex's $2.2 million list price for the cell product itself. In vivo editing dispenses with all of that: the editing machinery — typically packaged in a lipid nanoparticle (LNP), the same delivery technology that carried the mRNA COVID vaccines — is infused directly into the bloodstream and does its work inside the body. No conditioning, no cell manufacturing, no treatment-center bottleneck, at least in principle. The catch is biodistribution: LNPs traffic naturally to the liver, which is why every in vivo editing program furthest along in the clinic — Intellia/Regeneron's transthyretin amyloidosis program, CRISPR Therapeutics' CTX310 — targets a liver-expressed gene. Editing tissues the LNP does not naturally reach (muscle, brain, lung) remains a much harder unsolved delivery problem across the entire field.

2. CASGEVY: The Proof of Concept, Three Years In

By the numbers Vertex and CRISPR Therapeutics disclosed in their respective Q1 2026 reports, CASGEVY generated $43 million in recognised revenue for the quarter, with more than 500 patients having initiated therapy globally since launch. That is a small number in absolute dollar terms for a company the size of Vertex, but the more informative metric is the trajectory: Vertex management disclosed at its Q4 2025 call that CASGEVY had outpaced its closest competitor — Lyfgenia, bluebird bio's competing lentiviral gene therapy for sickle cell disease, which launched within a week of CASGEVY in December 2023 — by more than three-to-one on total authorized treatment starts over the first eight quarters on the market, despite Casgevy being the cheaper of the two therapies by list price. That is a genuinely useful data point: it suggests physicians and payers are not simply defaulting to whichever gene therapy arrived first, and that CRISPR-based editing's efficacy and safety profile is winning head-to-head share against an older gene-addition approach.

The pricing question deserves its own scrutiny, because it sits at the center of every bull and bear case for the ex vivo modality. The Institute for Clinical and Economic Review (ICER), the most influential independent health-economics body in US pharmaceutical pricing, concluded in its 2024 value assessment that CASGEVY's net health benefit — a functional cure for a disease that previously required lifelong transfusions, chelation therapy, and carried a materially shortened life expectancy — justified a price of up to approximately $2.05 million. Vertex's $2.2 million list price sits roughly 7% above that ceiling, which is a strikingly narrow gap for a first-in-class curative gene therapy; ICER's assessments for other gene therapies have found list prices two to three times above their calculated value-based ceilings. In plainer terms: independent health economists think CASGEVY is priced close to fairly, which is unusual in this category and probably helps explain the reimbursement agreements Vertex has been signing steadily through 2026, including a German GKV-Spitzenverband agreement finalized in the first quarter and continuing regulatory submissions to extend the label down into the 5-to-11 pediatric age band, with new data presented at the European Hematology Association Congress in June.

None of this changes the structural ceiling on how fast an ex vivo therapy can scale. Every patient needs a treatment-center slot, a four-to-six-month manufacturing turnaround, and a body healthy enough to tolerate myeloablative conditioning — which by itself excludes some of the sickest, most transfusion-dependent patients who arguably need the therapy most. The 500-patient initiation milestone at both companies' Q1 2026 disclosures should be read against an eligible population that runs into the hundreds of thousands of severe sickle cell and beta-thalassemia patients globally. Closing that gap is a manufacturing and healthcare-infrastructure problem as much as a commercial one, and it is the single most important operational variable for both stocks over the next several years.

3. Vertex Pharmaceuticals: The Cash Engine Behind the Platform

Vertex is worth understanding first as what it already is — the dominant franchise player in cystic fibrosis, having built and defended a near-monopoly in CFTR modulator therapy since KALYDECO's 2012 approval — before getting to what it is trying to become. That existing CF franchise is not a footnote to the CASGEVY story; it is the reason CASGEVY, JOURNAVX, and the rest of Vertex's diversification pipeline exist at all, funded entirely from CF cash flow without a single dilutive equity raise.

The numbers. Vertex reported Q1 2026 total product revenue of $2.99 billion, up 8% year-over-year, with non-GAAP EPS of $4.47 against a Street estimate of $4.33. Full-year 2026 guidance sits at $12.95–13.1 billion in total revenue, including more than $500 million from products outside the CF franchise for the first time — CASGEVY and JOURNAVX combined contributed roughly a quarter of the quarter's year-over-year growth. JOURNAVX (suzetrigine), Vertex's first-in-class, non-opioid NaV1.8 sodium-channel inhibitor for acute pain, is arguably the more commercially significant near-term story: it filled more than 350,000 prescriptions in Q1 2026 alone, versus roughly 550,000 for all of 2025, with payer coverage now extending to 240 million covered lives. A genuinely differentiated non-opioid option for acute pain, launched into a healthcare system still reckoning with the opioid crisis, has an obvious and large addressable market if the prescribing momentum holds.

The pipeline beyond CF and pain. Three assets define Vertex's next five years. Zimislecel, a stem-cell-derived, fully differentiated pancreatic islet cell therapy, aims to restore endogenous insulin production in type 1 diabetes — its pivotal Phase 3 study is fully enrolled, though Vertex disclosed a temporary pause in completing dosing pending an internal review, a detail worth tracking closely given how central this program is to the "Vertex beyond CF" bull thesis. Povetacicept, an engineered dual APRIL/BAFF antagonist, is Vertex's most clinically advanced non-CF asset: the FDA accepted its Biologics License Application for accelerated approval in IgA nephropathy in June 2026, it carries US Fast Track designation in primary membranous nephropathy and EMA PRIME designation, and Vertex has opened an additional Phase 2 study in generalized myasthenia gravis — an unusually broad autoimmune development program for a single molecule. Inaxaplin, an oral small-molecule APOL1 inhibitor, targets APOL1-mediated kidney disease, a genetically defined nephropathy disproportionately affecting patients of West African ancestry with no approved disease-modifying therapy today; the Phase 2/3 AMPLITUDE interim-analysis cohort completed enrollment in the second half of 2025, with data expected in early 2027.

The reminder that pipelines are not free options. The single largest one-day move in VRTX shares over the trailing year was a roughly 21% decline on August 5, 2025, triggered by a failed Phase 2 study of VX-993 — an oral, next-generation NaV1.8 pain candidate — in post-bunionectomy acute pain, which missed statistical significance on its primary endpoint, compounded by unchanged full-year guidance that disappointed investors positioned for an upward revision. It is a useful corrective to any narrative that treats Vertex as a low-risk compounder: even a company with this much commercial durability in CF trades meaningfully on pipeline read-through in adjacent indications, and single-asset Phase 2 failures can move a $125 billion market cap by a fifth in a single session.

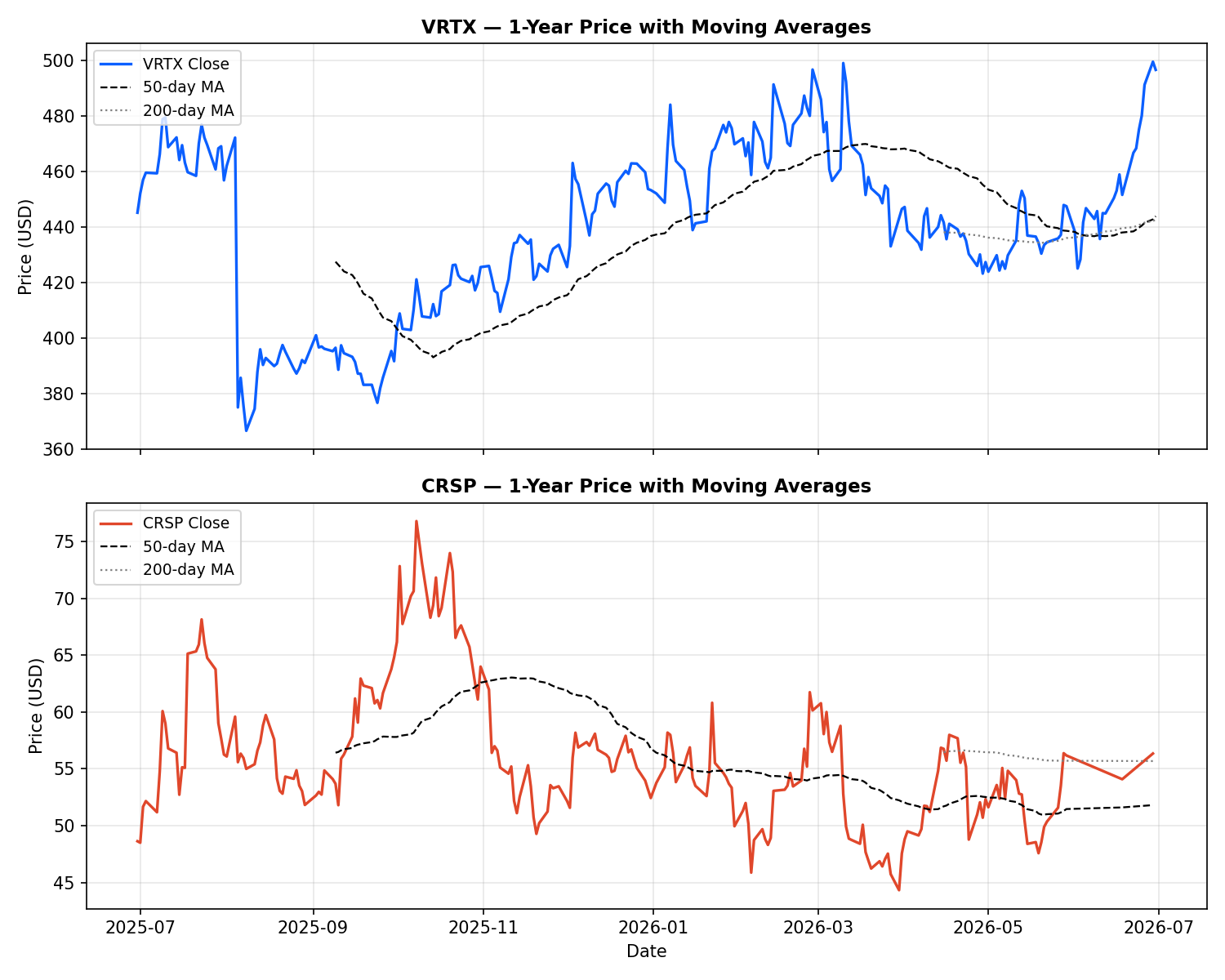

VRTX (top) and CRSP (bottom), daily close with 50-day and 200-day moving averages, trailing 12 months through June 30, 2026. Note the August 2025 gap-down in VRTX and CRSP's broader October 2025 peak and subsequent range-bound consolidation.

At current levels, VRTX trades around $497, roughly 9.8% below the Street's consensus 12-month price target of $548.69, with a trailing P/E of 29.6x and a forward P/E of 25.5x — a premium to the broader pharmaceutical sector that the market is willing to pay for CF's durability and the optionality in pain, kidney, and hematology. Individual analyst targets range unusually widely for a company this size, from $436 (Canaccord, Hold) to $616 (Morgan Stanley, Overweight) and $615 (Barclays), which tells you the Street itself is divided on how much credit to give the non-CF pipeline today versus waiting for data.

4. CRISPR Therapeutics: The Platform Company Behind the Platform

CRISPR Therapeutics is a different animal entirely — a pure-play gene-editing company whose CASGEVY economics are structured as a profit/loss share with Vertex rather than direct revenue recognition, meaning its own income statement will always look thin relative to the franchise's real commercial momentum. Full-year 2025 revenue was $3.51 million (down 90.6% year-over-year, reflecting the lapping of one-time collaboration payments from 2024), against a net loss of $581.6 million, 58.8% wider than the prior year. For a company at this stage, the balance sheet — not the income statement — is the fundamental that matters: CRSP held $2.44 billion in cash and investments as of March 31, 2026, freshly bolstered by a $600 million convertible senior notes offering (due 2031, 1.7308% coupon, ~$585.4 million net proceeds) completed during the quarter. That gives the company multi-year runway to fund CASGEVY-adjacent commercial infrastructure and a broadening in vivo and siRNA pipeline without near-term reliance on further dilutive equity — a materially stronger financial position than the company has held historically.

The pipeline that will decide whether CRSP is a royalty stream or a platform company. CTX310, an in vivo, LNP-delivered CRISPR/Cas9 therapy targeting ANGPTL3 in hepatocytes, is the most clinically de-risked non-CASGEVY asset in the portfolio. Phase 1 data showed dose-dependent, durable reductions with a single administration — up to an 89% maximum reduction in circulating ANGPTL3, 84% in triglycerides, and 87% in LDL cholesterol at the highest dose tested — positioning it as a potential one-time treatment for severe dyslipidemia and cardiovascular risk reduction, in direct competition with Intellia/Regeneron's in vivo cardiovascular franchise as well as non-editing siRNA and antisense approaches from other developers targeting the same pathway. CTX611 is a partnered siRNA asset targeting Factor XI, an anticoagulation-pathway target that rounds out a cardiovascular-focused in vivo franchise distinct in mechanism from CTX310. Zugo-cel, an allogeneic (off-the-shelf, non-patient-specific) CD19-directed CAR-T therapy, has been expanded from its original oncology indications into autoimmune disease — part of a broader industry-wide trend of testing CAR-T platforms in B-cell-driven autoimmune conditions like lupus, where early academic data across the field has been striking enough to draw serious pharma investment. Management has guided to multiple Phase 1/2 readouts across these programs in the second half of 2026, with pivotal trial starts targeted for 2027.

At current levels, CRSP trades around $56, with a Street consensus price target of $83.52 — implying roughly 48% upside, nearly five times the percentage upside embedded in VRTX's consensus target, which is exactly what you would expect from a pre-profitability platform company where the bull case runs through binary pipeline catalysts rather than compounding cash flow. 72% of covering analysts rate the stock Buy against 28% Hold, with zero Sell ratings — a distribution that reads as broad conviction in the underlying science tempered by genuine uncertainty about commercial execution timing.

5. The Competitive Field: Who Else Is Building This

Intellia Therapeutics, partnered with Regeneron, holds the most clinically advanced in vivo editing portfolio outside CRISPR Therapeutics' cardiovascular programs. Nexiguran ziclumeran (nex-z, NTLA-2001) is being developed for transthyretin amyloidosis (ATTR) across two indications — cardiomyopathy and polyneuropathy — with the polyneuropathy Phase 3 study (MAGNITUDE-2) having had a clinical hold lifted by the FDA in Q1 2026 and enrollment completion targeted for the second half of the year; a BLA filing is anticipated by 2028. More immediately significant: Intellia's other in vivo editing program, lonvoguran ziclumeran (lonvo-z) for hereditary angioedema, reported positive Phase 3 results from its HAELO study in April 2026 — a milestone Intellia and much of the trade press described as a global first for an in vivo CRISPR editing program to succeed in a registrational Phase 3 trial. If that holds up through regulatory review, it would be the second FDA approval pathway for CRISPR-based medicine after CASGEVY, and the first for the in vivo delivery paradigm — arguably a bigger structural validation for the sector's next decade than CASGEVY's ex vivo approval was, precisely because in vivo editing is the modality with the larger addressable-population ceiling.

Beam Therapeutics has differentiated on base-editing technology rather than nuclease editing, with three candidates in Phase 1/2 across sickle cell disease, alpha-1 antitrypsin deficiency, and glycogen storage disease 1a. Editas Medicine made the starkest strategic pivot in the sector, restructuring in December 2024 to abandon ex vivo commercialization entirely — walking away from its own sickle cell program — to concentrate exclusively on in vivo editing, a bet that extended its cash runway into Q2 2027 while it seeks human proof-of-concept. Whether that bet pays off is one of the more interesting open questions in the sector: it is a vote of confidence that in vivo delivery is close enough to clinical maturity to justify abandoning a nearer-term ex vivo commercial opportunity, from a company with direct visibility into where the delivery science actually stands.

6. A Full Year of Chart Data

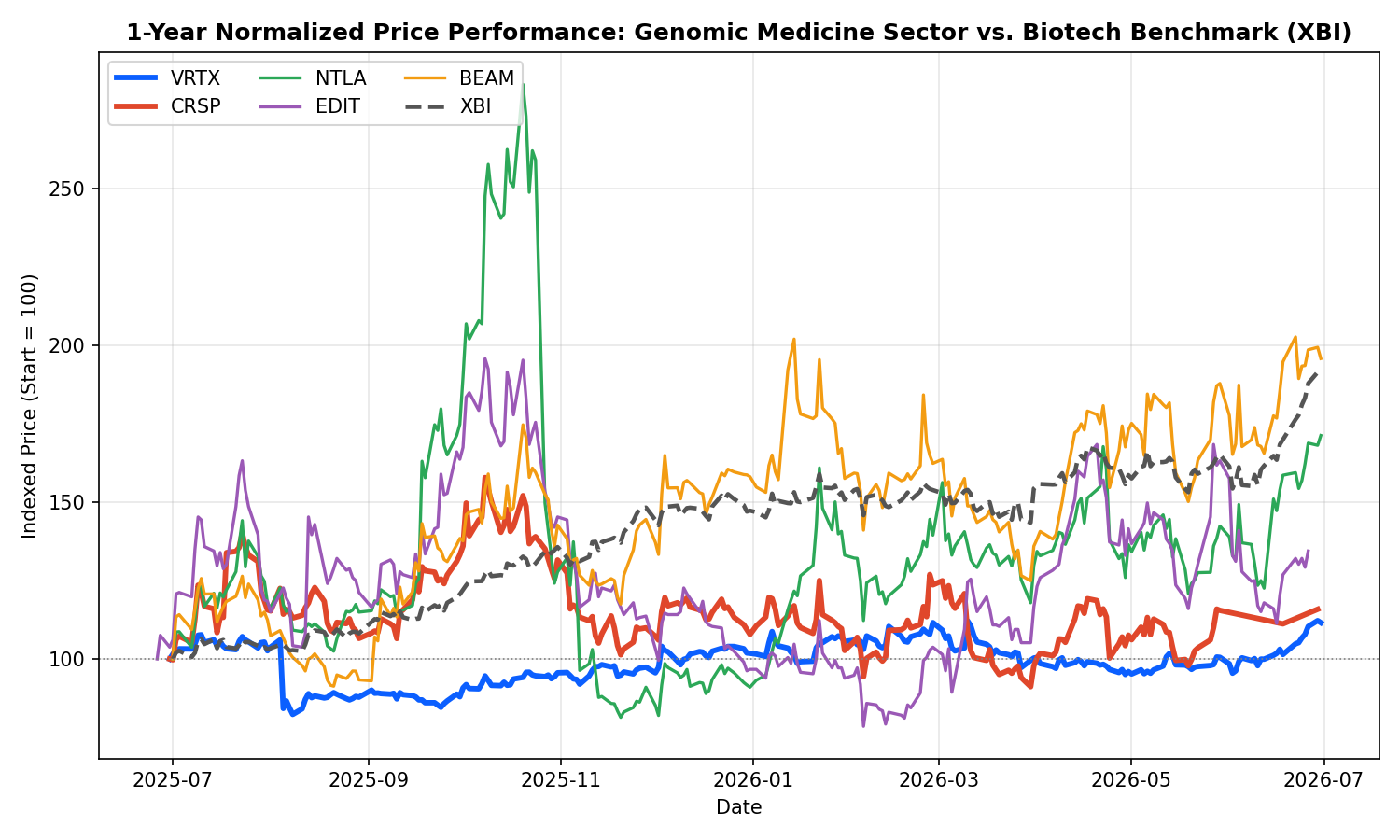

The chart below indexes VRTX, CRSP, and four reference securities — Intellia (NTLA), Editas (EDIT), Beam (BEAM), and the SPDR S&P Biotech ETF (XBI) as a sector benchmark — to 100 at the start of the trailing 52-week window (July 2025–June 2026).

Two things stand out. First, dispersion within the gene-editing cohort itself is wide — BEAM (+95.8%) and NTLA (+71.3%) meaningfully outperformed CRSP (+15.8%) and EDIT (+34.4%) despite all four companies operating in the same technology category, which tells you program-specific clinical readouts, not sector sentiment, are the dominant driver of individual stock returns right now. Second, both VRTX and CRSP underperformed the XBI benchmark (+91.3%) over the period — a function of both companies' starting valuations already pricing in a real, de-risked commercial asset (CASGEVY), which leaves less room for the sharp multiple re-ratings that reward earlier-stage peers off binary catalysts.

| Ticker | 1-Yr Return | 52-Wk Range | Ann. Volatility | Max Drawdown |

|---|---|---|---|---|

| VRTX | +11.6% | $362.50–$507.92 | 35.7% | −23.6% |

| CRSP | +15.8% | $44.12–$78.48 | 62.5% | −42.3% |

| NTLA | +71.3% | $7.95–$28.25 | 104.0% | −71.3% |

| EDIT | +34.4% | $1.66–$4.54 | 91.2% | −59.9% |

| BEAM | +95.8% | $15.60–$36.88 | 74.1% | −38.2% |

| XBI (benchmark) | +91.3% | $82.04–$160.01 | 26.6% | −9.7% |

VRTX sits in the lower-left of any risk/return plot of this group — below-benchmark volatility, below-benchmark return, the profile of a large-cap, cash-generative pharmaceutical company rather than a clinical-catalyst-driven biotech. CRSP sits closer to the benchmark on volatility but well below it on return, reflecting a company that is de-risked relative to its smaller peers by CASGEVY but has not yet been rewarded with a re-rating on pipeline optionality the way BEAM and NTLA have. (Price history sourced from StockAnalysis.com, underlying data via S&P Global Market Intelligence and CBOE; statistics computed on adjusted close over the trailing 365 days through June 29–30, 2026.)

7. Where This Goes

The next 18 months in genomic medicine will be decided less by whether the science works — CASGEVY, nex-z's Phase 1 data, lonvo-z's Phase 3 win, and CTX310's Phase 1 lipid data have each already cleared that bar for their respective modalities — and more by commercial execution and capital discipline. For Vertex, the open questions are whether non-CF revenue can scale fast enough to offset the eventual maturation of the CF franchise that funds everything else, and whether the pipeline can avoid further binary disappointments of the VX-993 variety while povetacicept, inaxaplin, and zimislecel work through their respective regulatory paths. For CRISPR Therapeutics, the questions are whether CASGEVY's patient-initiation rate can meaningfully accelerate against its structural ex vivo bottlenecks, and whether CTX310's promising Phase 1 biomarker data can translate into a differentiated Phase 3 cardiovascular program ahead of well-funded competitors — Intellia and Regeneron chief among them.

My own reading, as someone who trained in medicine before spending the last several years close to the applied AI and biotech data side of this industry: the ex vivo/in vivo split happening across this sector right now rhymes with a pattern I have seen before in other parts of medicine — a first-generation technology proves the biology works in the hardest, highest-unmet-need population, at high cost and low throughput, and creates the regulatory and reimbursement pathway that a more scalable second-generation technology then walks through. CASGEVY did that job. Whether Intellia's lonvo-z, CRISPR Therapeutics' CTX310, or a program not yet in the clinic ends up being genomic medicine's second act at real population scale is the single most interesting open question in biotech today, and it is one worth watching closely over the next several data readouts rather than trading on any single quarter's headline.

This article is a research and educational summary and does not constitute investment advice. It is not a recommendation to buy or sell any security. Readers should consult a licensed financial advisor and conduct independent due diligence before making investment decisions. Historical performance is not indicative of future results.

References and Further Reading

- Vertex Pharmaceuticals — Q1 2026 Financial Results — company press release and investor materials

- CRISPR Therapeutics — Q1 2026 Business Update and Financial Results — company press release and investor materials

- ICER — Sickle Cell Disease Gene Therapy Value Assessment — independent cost-effectiveness analysis of CASGEVY and Lyfgenia

- CRISPR Therapeutics — CTX310 Phase 1 Data (ANGPTL3) — press release with full Phase 1 biomarker data

- Intellia Therapeutics — HAELO Phase 3 Results (lonvoguran ziclumeran) — press release on hereditary angioedema Phase 3 data

- Intellia Therapeutics — MAGNITUDE-2 Phase 3 Update (nexiguran ziclumeran) — ATTR amyloidosis polyneuropathy trial status

- Beam Therapeutics — Base Editing Platform Overview — technical explainer on base editing mechanism

- StockAnalysis.com — VRTX and CRSP — price history, fundamentals, and analyst estimates used throughout this article

- The Nobel Prize in Chemistry 2020 — Jennifer Doudna and Emmanuelle Charpentier, "for the development of a method for genome editing"