In January 1848, a carpenter named James Marshall found flecks of gold in the tailrace of a sawmill on the American River in California. Within eighteen months, roughly 300,000 people had uprooted their lives and crossed a continent — or sailed around Cape Horn — to dig for it. Almost none of them got rich. The people who reliably got rich were the ones who sold the diggers what they needed to keep digging: Levi Strauss sewed canvas trousers, Studebaker built wheelbarrows, and a small express company called Wells, Fargo & Co. moved the gold and the money once it existed. The gold rush made a handful of miners wealthy by luck and made an entire supply chain wealthy by arithmetic.

I open with that story because I think it is the correct lens for what has happened to memory and storage stocks over the past twelve months, and I want to be direct about why I am writing this: I believe the current pullback in this sector is a buying opportunity, not a warning sign, and I want to walk you through the data that leads me there — company by company, with the same depth I gave Vertex and CRISPR Therapeutics in my last markets piece. I also want to be upfront that I help people think through exactly this kind of decision for a living, and if you want to talk through position sizing or actually opening these positions, that offer is at the bottom of this piece, not hidden in it.

1. The Setup: What Actually Happened to Memory Prices

The proximate cause of everything in this article is unglamorous: the world does not have enough NAND flash or DRAM to satisfy simultaneous demand from AI data centers, which need staggering quantities of high-bandwidth memory (HBM) and enterprise SSD capacity, and the ordinary consumer electronics industry, which still needs the same wafers it always needed for phones, laptops, and cars. Years of underinvestment during the 2022–2024 memory downturn — when oversupply crushed prices and manufacturers cut capital spending to protect margins — left the industry with too little fabrication capacity right as AI infrastructure buildouts went vertical. Micron's own CEO, Sanjay Mehrotra, said as much on June 30: customers' aggressive price negotiating during the downturn left the industry underinvested just before AI demand surged, and that mismatch is the shortage playing out today.

The clearest evidence of how serious this has become is that it is now visibly hitting consumers. On July 1, Apple CEO Tim Cook told the Wall Street Journal that price increases across Apple's product line are "unavoidable," comparing the memory shortage to a "hundred-year flood." TechInsights has estimated the cost of the next iPhone Pro could rise by more than $200 as a direct result. Apple has reportedly gone as far as exploring purchases from Chinese memory makers on a Pentagon blacklist to plug the gap — a sign of how little slack exists in the global supply chain right now. When a company with Apple's negotiating leverage and balance sheet is forced to publicly warn customers about price increases, that is a company confirming, in the most costly way possible, that its suppliers have pricing power they have not had in a decade.

That pricing power is the entire investment thesis for this article.

2. SanDisk and Western Digital: The Direct Beneficiaries

A tale of one spin-off

SanDisk (NASDAQ: SNDK) is, technically, a one-year-old public company — it was spun out of Western Digital (NASDAQ: WDC) in February 2025, splitting a combined hard-disk-and-flash business into a pure-play NAND flash company (SanDisk) and a pure-play hard-disk-drive company (Western Digital). Both halves of that split have turned out to be extraordinarily well-timed, because both NAND flash and hard-disk-drive capacity are now scarce inputs into the same AI buildout.

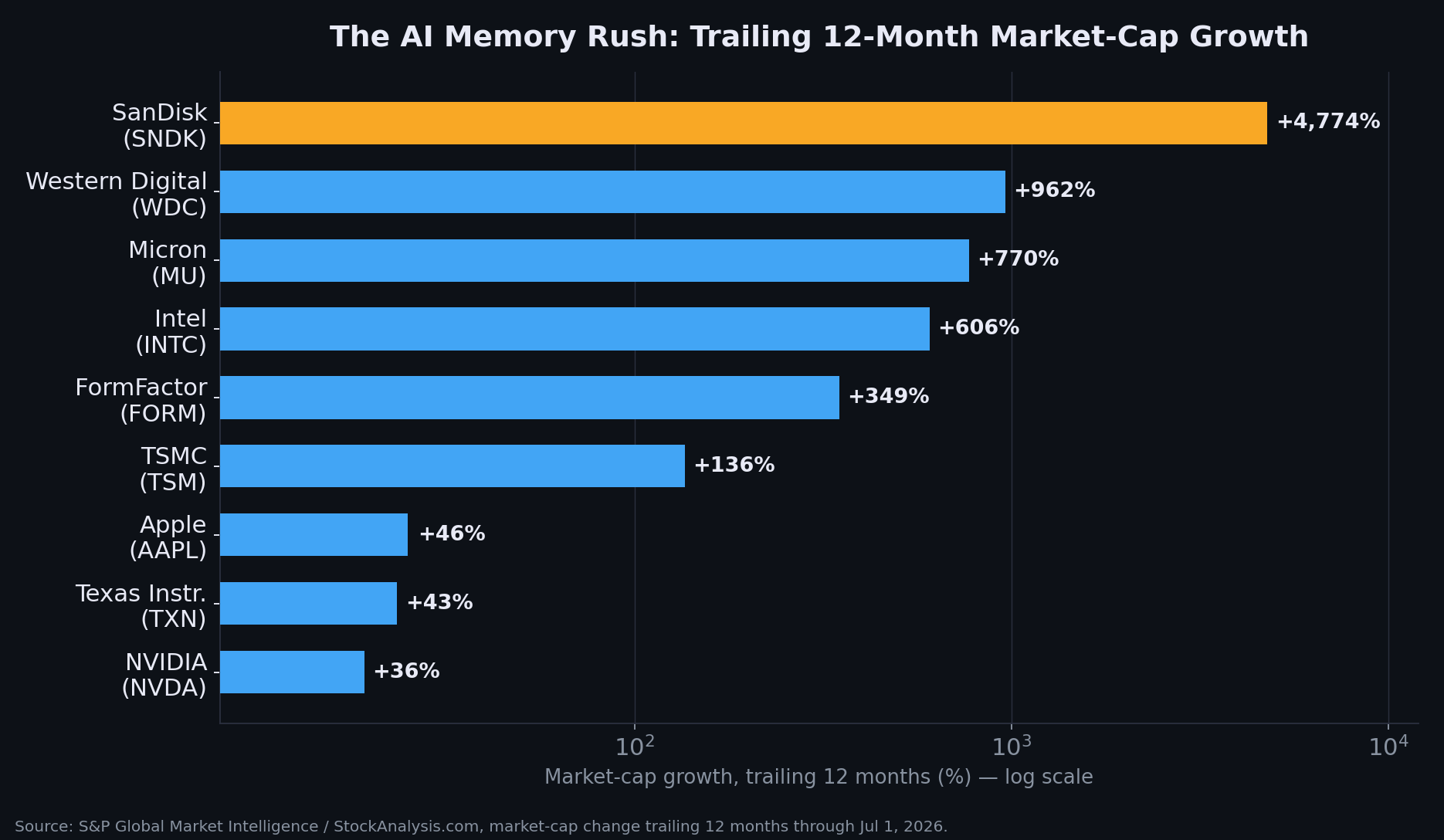

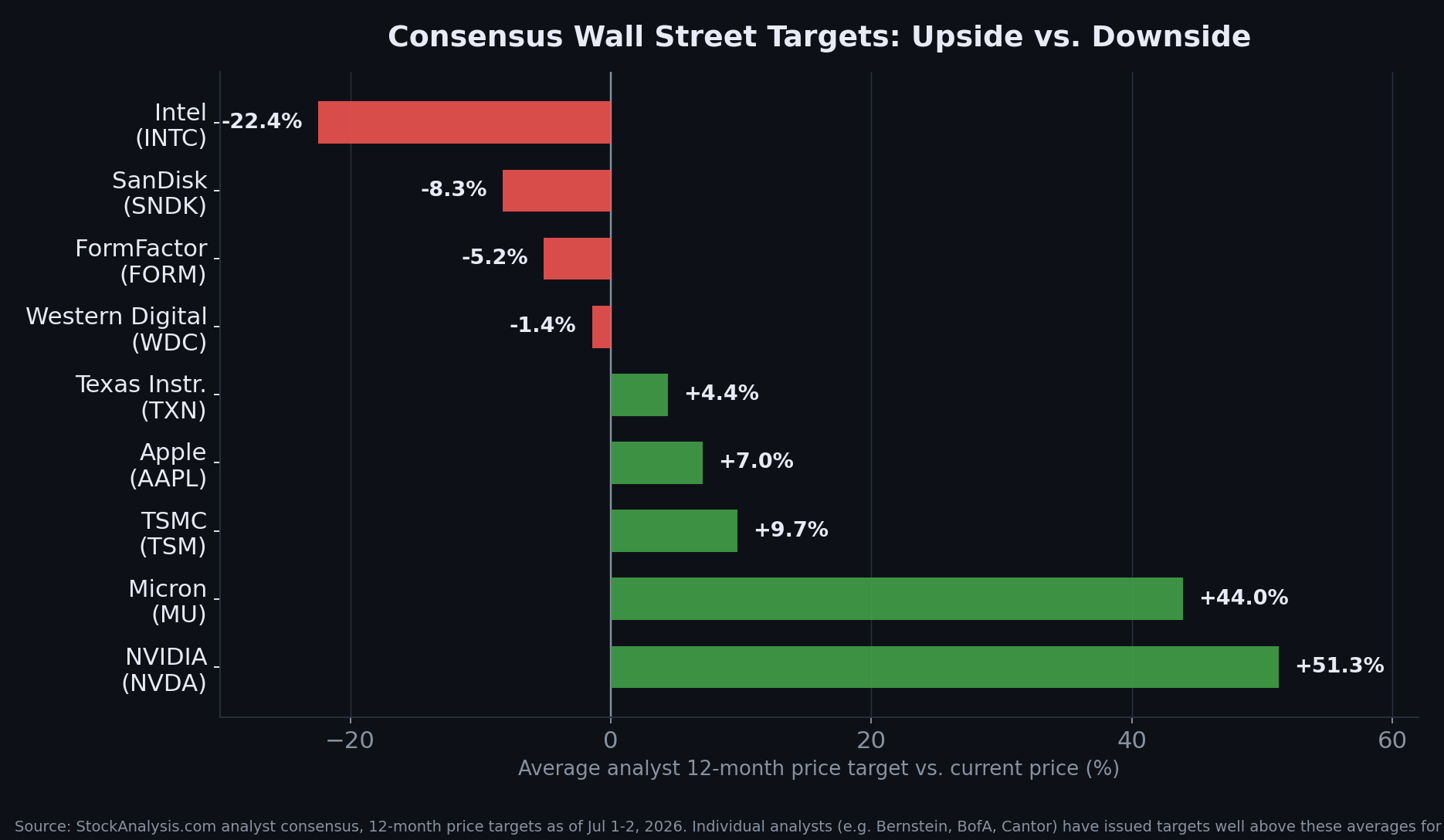

SanDisk's numbers, plainly stated: the stock closed July 1 at $2,032.22, after falling 10.6% that session — but that single ugly day sits on top of a move that is difficult to describe without sounding like a typo. SanDisk's market capitalization is up 4,774% over the trailing twelve months, and multiple outlets (TipRanks, Invezz) independently reported the stock up somewhere between 780% and 800% year-to-date in 2026 alone, before the July pullback. The 52-week range is $40.10 to $2,354.39. Sell-side analysts have been racing to keep up: Bernstein's Mark Newman raised his price target from $1,700 to $3,000 on June 30, calling SanDisk's supply contracts "more powerful" than the market appreciates, and Bank of America raised its target to $2,500 from $2,100 the same week — even as the stock was falling on the day of the upgrade, which tells you the drop was a sentiment and positioning event, not a change in anyone's view of the underlying business. The average of 22 analysts still lands at $1,863.82, which is technically below the current price, and I will come back to why that gap matters in the risks section below.

Western Digital's numbers: WDC closed July 1 at $598.37, down 6.3% on the day, against a 52-week range of $62.94 to $799.87. It set an all-time high on June 18 — meaning the stock is now roughly 25% below where it traded just two weeks ago, the steepest drawdown of any name in this piece. Year-to-date, WDC is up 264%; over the trailing twelve months, market cap is up 961.5%. Melius Research initiated coverage in late June with a Buy rating and a $1,050 price target — nearly double where the stock trades today — explicitly framing Western Digital as "AI infrastructure" exposure rather than a legacy hard-drive company. Cantor Fitzgerald raised its target to $900 from $660 the same week, and Bank of America moved to $732 from $610. Not every analyst agrees: Fox Advisors downgraded WDC to Equal-Weight in late June, arguing that expectations for further hard-disk-drive price increases "may be getting ahead" of what is actually likely — a reasonable caution I'll weigh in Section 6.

The chart below shows just how far outside the normal range of stock market outcomes this move has been, plotted on a log scale because a linear scale cannot fit SanDisk's bar on the same page as everything else.

Trailing 12-month market-cap growth across the group. SanDisk and Western Digital sit at the extreme end of a genuinely unusual sector-wide move. Source: S&P Global Market Intelligence via StockAnalysis.com.

Why the fundamentals are catching up, not just the multiple

It would be a much weaker thesis if this were pure multiple expansion. It isn't. SanDisk's trailing-twelve-month revenue is $13.18 billion, up 82.8% year-over-year, with a forward P/E of just 11.88 despite the share price move — the market is pricing in continued, not peaking, earnings growth. Western Digital's numbers are, if anything, more striking on the profitability side: trailing revenue of $11.78 billion (+32.0%), net income of $6.38 billion (+295.6% year-over-year), and EPS of $18.35, up 302.7%. This is a company whose earnings are compounding roughly as fast as its stock price, which is unusual for a stock that has gone up nearly tenfold.

3. The Pullback, Sized Honestly

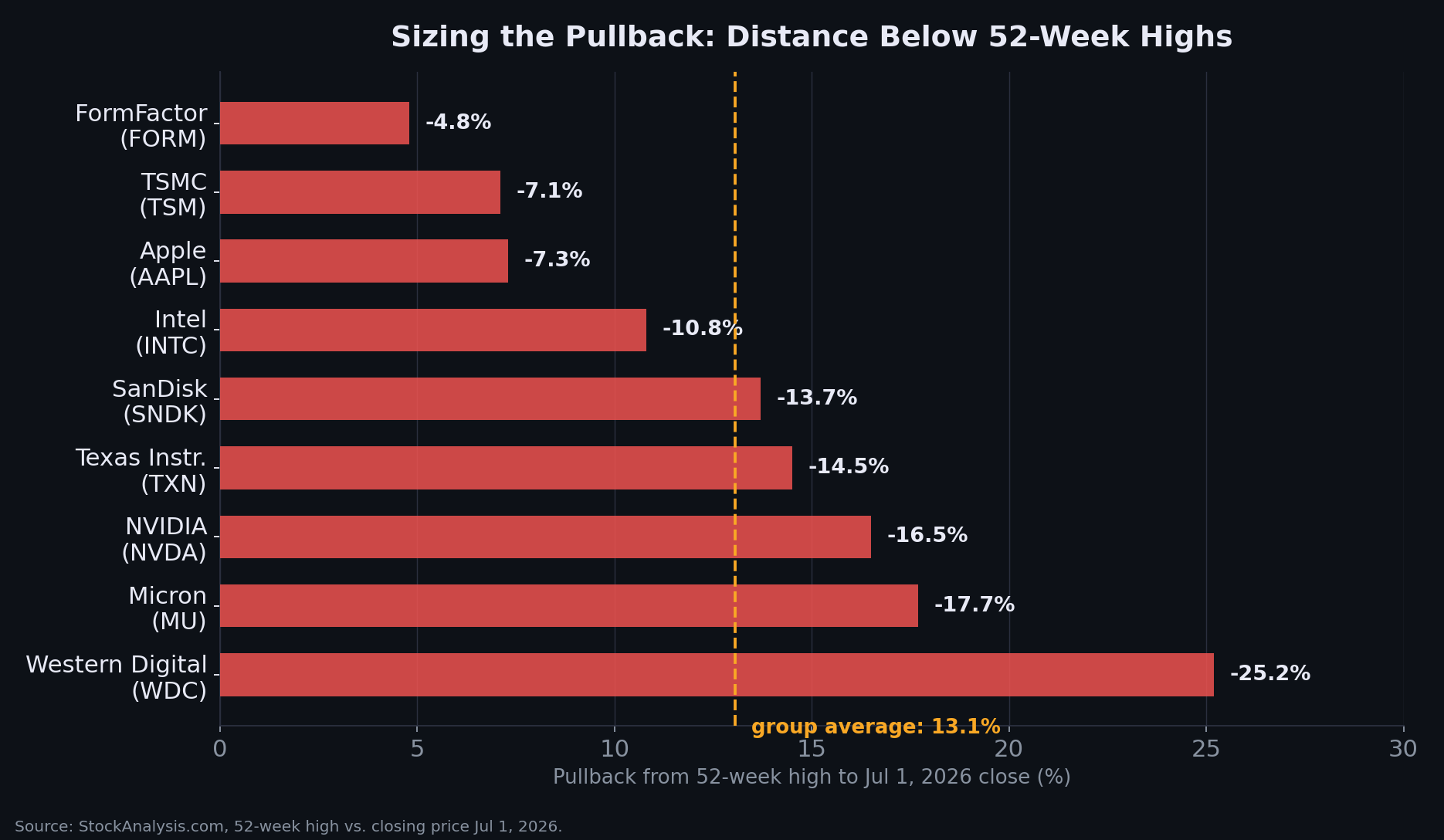

I don't want to undersell what happened on July 1. It was the worst single day for chip and memory stocks since the rally began, and it followed a second quarter in which Micron, Intel, and AMD alone added roughly $2 trillion in combined market value — a figure CNBC and TipRanks both flagged as historic. Profit-taking after a quarter like that was inevitable; the only question was timing. SanDisk fell 10.6%, Micron fell 10.6%, Intel fell 9.0%, TSMC fell 6.8%, Western Digital fell 6.3%, and FormFactor fell 4.6%, all in the same session, as reported across MarketWatch, Invezz, and CNBC.

Measuring from each stock's 52-week high rather than a single bad day gives a cleaner picture of how much air has actually come out of the trade:

Distance below 52-week highs as of the July 1, 2026 close. The group average of 13.1% is close to the "about 10%" figure most financial media used to describe the sector move, though individual names range from a shallow 4.8% (FormFactor) to a much sharper 25.2% (Western Digital).

The reason I don't read this as the beginning of the end is that the driver of the rally — physical scarcity of NAND and DRAM capacity — has not changed. MarketWatch's own headline on the sell-off put it plainly: "SanDisk's and Micron's stocks sink as the rotation trade builds, but supply shortages should limit losses." A rotation out of a crowded trade on valuation concerns is a very different animal from a rotation out of a trade because the underlying story broke. Micron's fiscal Q3 2026 revenue, reported days before the pullback, came in at $41.46 billion — up nearly 350% year-over-year — and still triggered a relief rally in the whole memory complex before profit-taking set in. That is not the earnings print of a supply-demand imbalance that is closing.

4. The Rest of the Stack: Who Else Is Selling Picks and Shovels

SanDisk and Western Digital are the most direct plays on the memory shortage, but they sit inside a much larger AI hardware ecosystem, and I think it's worth understanding where each of the following names fits before deciding where your own capital should go.

NVIDIA (NASDAQ: NVDA) — the trade that's already priced for perfection

NVIDIA is the name most people mean when they say "AI stock," and it remains the largest company in the group by a wide margin — a $4.79 trillion market cap, up 35.5% over the trailing twelve months, on trailing revenue of $253.5 billion (+70.7%) and net income of $159.6 billion (+107.9%). Those are extraordinary absolute numbers. But the relative story in 2026 has been a genuine surprise: NVIDIA closed July 1 at $197.58, down from a 52-week high of $236.54 set on May 14 — a 16.5% pullback — and Barron's flagged in late June that NVIDIA stock is "trailing chip rivals" in 2026, lagging far behind the roughly 94% gain in the PHLX Semiconductor Index for the year. The market has, in effect, already priced NVIDIA's AI dominance in and moved on to hunting for the next re-rating candidate — which is precisely why capital has rotated so hard into memory, storage, and testing names instead. Analysts remain bullish (Strong Buy consensus, average target $301.62, implying over 51% upside), but that upside case now depends more on continued execution — the Vera Rubin platform, the Palantir partnership, the physical-AI and robotics narrative Jensen Huang has been pushing — than on a re-rating from a low starting valuation. Worth noting for balance: investor Michael Burry disclosed a fresh short position against NVIDIA in late June, alongside shorts on Tesla, Caterpillar, and Applied Materials, citing broader AI-valuation concerns.

TSMC (NYSE: TSM) — the chokepoint everyone depends on

Taiwan Semiconductor is, in a real sense, the actual gold mine underneath this entire boom: essentially every advanced AI chip in the world — NVIDIA's, Apple's, AMD's — is fabricated in a TSMC facility, because no other foundry can match its leading-edge process nodes and advanced packaging capacity at scale. TSMC closed July 1 at $445.12 (-6.8% on the day, -7.1% from its 52-week high of $479.00), with a market cap of $2.04 trillion, up 135.7% over the trailing year. The company has forecast full-year 2026 revenue growth above 30%, and CEO C.C. Wei has said publicly that AI chip demand will outpace TSMC's supply "for years to come" — CoWoS advanced-packaging capacity, the bottleneck technology behind HBM integration, is expected to grow at more than an 80% compound annual rate from 2022 to 2027. Analyst consensus is Strong Buy, with an average target of $487.56 (+9.7%) and UBS at the high end targeting the equivalent of roughly $600+ on continued AI packaging strength. If SanDisk and Western Digital are the AI boom's raw-material sellers, TSMC is the one company nobody in the entire AI supply chain can route around.

Intel (NASDAQ: INTC) — the turnaround with government backing

Intel is the highest-variance story in this piece. The stock started 2026 near $37 and traded as high as $142.35 before closing July 1 at $127.02 (-9.0% on the day), a market cap of $638.4 billion that has grown 605.7% over the trailing twelve months. That move reflects a genuine business inflection: Intel's 18A-P leading-edge manufacturing node entered risk production on schedule, and the company has landed foundry backing and customer commitments from NVIDIA, SoftBank, and the U.S. government, positioning Intel as a credible second source for advanced chip manufacturing outside TSMC — a strategically important role given how concentrated the industry has become in Taiwan. Reports that Google and NVIDIA may use Intel as a backup manufacturer triggered an 11% single-day surge in June. But the financial reality underneath the stock price is still rough: Intel posted a net loss of roughly $3.17 billion on the trailing twelve months, and analyst sentiment is genuinely split — the average consensus rating is Hold with an average price target of $98.50, implying more than 22% downside from current levels, even as individual bulls like Cantor Fitzgerald ($150 target) and Bank of America ($160 target) see meaningfully more room to run. This is the one name in the piece I'd flag as a turnaround bet layered on top of an AI-infrastructure bet, not a pure-play on the shortage.

Micron (NASDAQ: MU) — the memory bellwether

If SanDisk is the NAND flash story, Micron is the broader memory bellwether that moves the whole complex — it makes both DRAM and NAND, and its earnings prints have repeatedly been the catalyst for rallies (and now, sell-offs) across SanDisk, Western Digital, and Seagate. Micron closed July 1 at $1,032.28 (-10.6%, and -17.7% from its June 25 all-time high of $1,213.56), with a market cap of $1.17 trillion, up 770.5% over the trailing year and roughly 280% year-to-date — the second-best-performing stock in the entire S&P 500 in 2026. Fiscal Q3 revenue of $41.46 billion, up nearly 350% year-over-year, is the single earnings print most responsible for reigniting the whole memory trade in late June. Micron also just signed a strategic supply agreement with General Motors for automotive memory and storage, diversifying its AI-data-center-heavy revenue base, and committed $250 million to the new "Trump Accounts" children's savings program. Analyst consensus is Strong Buy with an average target of $1,486 (+44% upside) — among the more bullish setups in this entire piece by that metric. The obvious risk: Samsung, SK Hynix, and Micron are now facing a U.S. class-action lawsuit alleging DRAM price coordination, filed as the shortage narrative reached a fever pitch — worth watching, not yet resolved.

FormFactor (NASDAQ: FORM) — the small, unglamorous chokepoint

FormFactor is the name in this piece most people have never heard of, and it may be the purest "picks and shovels" play here. It makes probe cards — the hardware used to test semiconductor wafers, including DRAM and HBM, before they're packaged — and it is the number-one global supplier in that category, with SK Hynix, the dominant HBM producer, as a key customer. FormFactor closed at $152.54 on July 1 (-4.6%, the shallowest pullback of any name here, at just 4.8% off its 52-week high), with a market cap up 349.1% over the trailing year. Q1 2026 revenue rose 32% to $226.1 million and net income tripled, driven by HBM3E and early HBM4 probe-card demand. Management has laid out a plan to double revenue to $1.6 billion by 2030. It's a smaller, more volatile stock than the others in this piece — market cap under $12 billion, versus trillions for TSMC and NVIDIA — but it captures AI memory demand without taking on SanDisk or Micron's direct commodity-pricing exposure.

Texas Instruments (NASDAQ: TXN) — the power behind the rack

Texas Instruments doesn't make memory or logic chips for AI models — it makes the analog and power-management chips that get AI data centers electricity in a usable form, and that business has been quietly reaccelerating. TXN's data center revenue grew 90% year-over-year in Q1 2026, now 11–12% of total sales, driven by the re-architecture of power distribution inside AI server racks. The stock closed at $285.48 on June 29, up a modest 43.2% in trailing market cap terms — genuinely staid compared to everything else in this piece — but that quarter's earnings beat sent the stock up 18% in a single day in April, its best day since 2000. TI has reportedly planned analog chip price increases of up to 85% on some products starting in April 2026, driven by AI server, EV, and industrial demand. Analyst targets have been climbing steadily: BofA to $370, Stifel to $360, Seaport Research upgrading to Buy at $400. TXN is the least "story" stock in this piece and, partly for that reason, the one with the most analyst agreement that it's still undervalued.

Apple (NASDAQ: AAPL) — the AI boom's biggest customer, not its biggest winner

Apple belongs in this piece for a different reason than the others: it is simultaneously an AI compute company (Apple Silicon, the M-series and A-series chips fabricated by TSMC, and the Neural Engine driving Apple Intelligence) and the party absorbing the cost of the memory shortage rather than profiting from it. Apple closed July 1 at $294.38, up 1.7% on the day, with a market cap of $4.32 trillion (+45.9% trailing twelve months) — solid, unspectacular by the standards of this piece. Tim Cook's own comments about "unavoidable" price increases are the clearest evidence that Apple is a price-taker in this market, not a price-setter, on the memory and storage components that go into every iPhone, Mac, and iPad it sells. That's not a reason to avoid the stock — Apple's analyst consensus is Buy with a $315.09 target (+7.0%), and its underlying silicon strategy remains a genuine AI-compute moat — but in the specific context of this article, Apple is best understood as the AI boom's largest customer being squeezed by its own suppliers, which is a meaningfully different position than SanDisk, Western Digital, Micron, or FormFactor occupy.

Where Wall Street's average 12-month target sits relative to today's price. Note that consensus targets often lag fast-moving individual analyst upgrades — Bernstein's $3,000 SanDisk target, for instance, is far above the $1,863.82 group average shown here.

5. Company Snapshot

| Company | Ticker | Jul 1 Close | 52-Wk Range | Trailing Mkt-Cap Growth | Analyst Consensus | Avg. 12-Mo Target |

|---|---|---|---|---|---|---|

| SanDisk | SNDK | $2,032.22 | $40.10–$2,354.39 | +4,774% | Buy | $1,863.82 (-8.3%) |

| Western Digital | WDC | $598.37 | $62.94–$799.87 | +962% | Buy | $589.88 (-1.4%) |

| Micron | MU | $1,032.28 | $103.38–$1,255.00 | +771% | Strong Buy | $1,486.00 (+44.0%) |

| Intel | INTC | $127.02 | $18.97–$142.35 | +606% | Hold | $98.50 (-22.4%) |

| FormFactor | FORM | $152.54 | $26.08–$160.27 | +349% | Buy | $144.67 (-5.2%) |

| TSMC | TSM | $445.12 | $221.18–$479.00 | +136% | Strong Buy | $487.56 (+9.7%) |

| Apple | AAPL | $294.38 | $201.50–$317.40 | +46% | Buy | $315.09 (+7.0%) |

| Texas Instruments | TXN | $285.48* | $152.73–$334.03 | +43% | Buy | $298.00 (+4.4%) |

| NVIDIA | NVDA | $197.58 | $151.49–$236.54 | +36% | Strong Buy | $301.62 (+51.3%) |

TXN priced as of the June 29, 2026 close. All other prices as of the July 1, 2026 close. Source: StockAnalysis.com / S&P Global Market Intelligence.

6. What Could Go Wrong

I said at the outset that I think this pullback is a buying opportunity, and I stand by that. But the responsible version of that argument has to sit next to the case against it, so here is the honest bear case, drawn from the same reporting cited above rather than invented for balance.

Valuations have genuinely stretched. Barron's ran a piece in mid-June bluntly titled "Why It Is Time to Stop Buying Chip Stocks," noting that sales and profit estimates have moved higher across the sector, but valuations have expanded even faster, and volatility is picking up. That is a fair description of what a chart of any stock in this piece looks like.

Not every analyst agrees the story continues. Fox Advisors' downgrade of Western Digital cited concern that hard-disk-drive pricing expectations "may be getting ahead" of what's realistic — a specific, falsifiable worry about the WDC leg of this trade in particular. Intel's average analyst target sits 22% below the current price, which is a genuine, not cosmetic, disagreement among the 49 analysts who cover the stock.

Legal and regulatory risk is live. Samsung, SK Hynix, and Micron are defendants in a new U.S. class-action lawsuit alleging DRAM price coordination. If that suit gains traction, it could constrain the pricing power that is the entire basis of the memory-stock rally, or invite regulatory scrutiny that slows the supply response the market is counting on.

Prominent skeptics are positioned against the trade. Michael Burry — famous for the trade dramatized in The Big Short — disclosed fresh short positions against NVIDIA, Applied Materials, Tesla, and Caterpillar in late June, explicitly citing AI-valuation concerns. He is one voice, not an oracle, but he is a well-informed one, and dismissing him outright would be intellectually lazy.

The gold rush analogy cuts both ways. It's worth remembering that most of the 300,000 people who went to California in 1848–1855 lost money, worked brutal conditions, and went home poorer than they arrived. The people who made durable fortunes were disproportionately the suppliers — the picks-and-shovels sellers — rather than the miners chasing the next big strike. In this analogy, that arguably favors TSMC (the toll-taker every AI chip must pass through) and FormFactor (a specialized, hard-to-replace supplier) over the more commodity-like, historically boom-bust memory names like SanDisk, Western Digital, and Micron, whose entire histories — this is not their first cycle — have been defined by dramatic price spikes followed by dramatic price collapses once new capacity comes online. Nothing about physics prevents that from happening again in 2027 or 2028 once the current wave of fab investment matures into shipped wafers.

I don't think any of that changes the near-term picture — the shortage is real, the earnings are real, and the pullback looks more like profit-taking than a trend reversal — but a full accounting of the trade has to include it.

7. Where I Land

Gold rushes are, definitionally, once-in-a-generation events, and I don't think this one is over. The difference between 1848 and 2026 is that today's version comes with quarterly earnings reports, SEC filings, and twenty-two Wall Street analysts publishing price targets on every name — which means, unlike the forty-niners panning blind in a river, you can actually underwrite this decision with real data before you make it. That data currently shows a sector growing earnings roughly as fast as its share prices, a supply shortage with no credible near-term resolution, and a July 1 pullback that every piece of reporting I could find attributes to profit-taking and rotation rather than a broken thesis.

I've spent this piece walking through nine companies at the depth I think the decision deserves, because I don't think "buy AI stocks" is a serious recommendation — which specific company, at which valuation, with which risk profile, is the actual question, and the honest answer is different for a FormFactor position than for an Intel position.

If you want to talk through any of this in more depth — what position sizing makes sense for your own portfolio, how to think about entry points into names that have already moved this much, or actually placing the trades — that is exactly the kind of conversation I have with clients regularly, and I'm happy to have it with you too. Reach out here to set up a time.

This article is a research and educational summary and does not constitute investment advice, and I am not a licensed financial advisor. It is not a recommendation to buy or sell any security. Readers should consult a licensed financial advisor and conduct independent due diligence before making investment decisions. Historical and recent performance, including the extraordinary moves described above, is not indicative of future results — several of the percentage gains cited in this piece are among the largest ever recorded for stocks of this size, and reversion is a real possibility, not just a disclaimer.

References and Further Reading

- StockAnalysis.com — SNDK, WDC, MU, NVDA, TSM, INTC, TXN, FORM, AAPL — real-time prices, fundamentals, and analyst consensus used throughout this article

- MarketWatch — "Sandisk's and Micron's stocks sink as the rotation trade builds, but supply shortages should limit losses"

- CNBC — "Record chip rally adds $2 trillion in combined value to Micron, Intel and AMD in second quarter"

- TipRanks — "Bernstein Rockets SanDisk Price Target to $3,000"

- Invezz — "Soaring Western Digital stock faces some major risks: is a reversal coming?"

- ABC News / WSJ — Tim Cook on Apple price increases amid memory chip shortage

- Barron's — "Why It Is Time to Stop Buying Chip Stocks"

- Barron's — "Nvidia Stock Trails Chip Rivals in a Tough First Half"

- Business Insider — "'Big Short' investor Michael Burry reveals fresh bets against Tesla, Nvidia, and Caterpillar"

- Reuters — "Micron, GM sign semiconductor supply agreement for vehicles"

- Invezz — "Samsung, SK Hynix, Micron sued over DRAM prices: what's at stake"

- GlobeNewswire — FormFactor Investor Day 2026 transcript

- CNBC — "TSMC first-quarter profit rises 58%, beats estimates as AI demand fuels record run"